Page 8

— Multifamily Properties Quarterly — July 2015

Civil site services are often written off as a sim-

ple, commodity based component of a construc-

tion project. In contrast, these services literally

serve as the foundation to your project and de-

serve extensive attention. Fiore combines 5 de-

cades of experience with well-coordinated, high

quality, efficient, timely, and environmentally

conscious civil services to ensure that your proj-

ect is built on a rock solid base.

Our INNOVATIVE SOLUTIONS, STRATEGIC

PROBLEM SOLVING, and WIDE SCOPE OF SER-

VICES can be delivered fully managed, as a com-

bined package or stand alone to meet the needs

of the client and always come with our partner-

ship commitment to deliver more than what you

paid for.

Don’t build your next project on the cheapest dirt

and infrastructure you can buy - your entire proj-

ect literally depends on it!

Single services to full site

work packages

Site Management - Demolition

Earthwork - Site Utilities

Environmental - Land Development

Commercial - Landfill - Recycling

Now offering Complete Civil

Contracting Services

Together We Can Move Mountains

P

erhaps the biggest question

multifamily investors are

asking themselves as they

consider investment in the

Denver metro market is: Can

the multifamily market continue to

improve? After studying the funda-

mental supply-and-demand charac-

teristics of today’s market, we think

the answer is yes.

How can this be after we have seen

unprecedented rent growth, as well

as incredible levels of construction

of new multifamily properties over

the last half-decade? Our conclusion

is that the market will continue to

improve because there simply is not

enough housing to meet the metro

area’s pent-up, as well as continually

growing, demand.

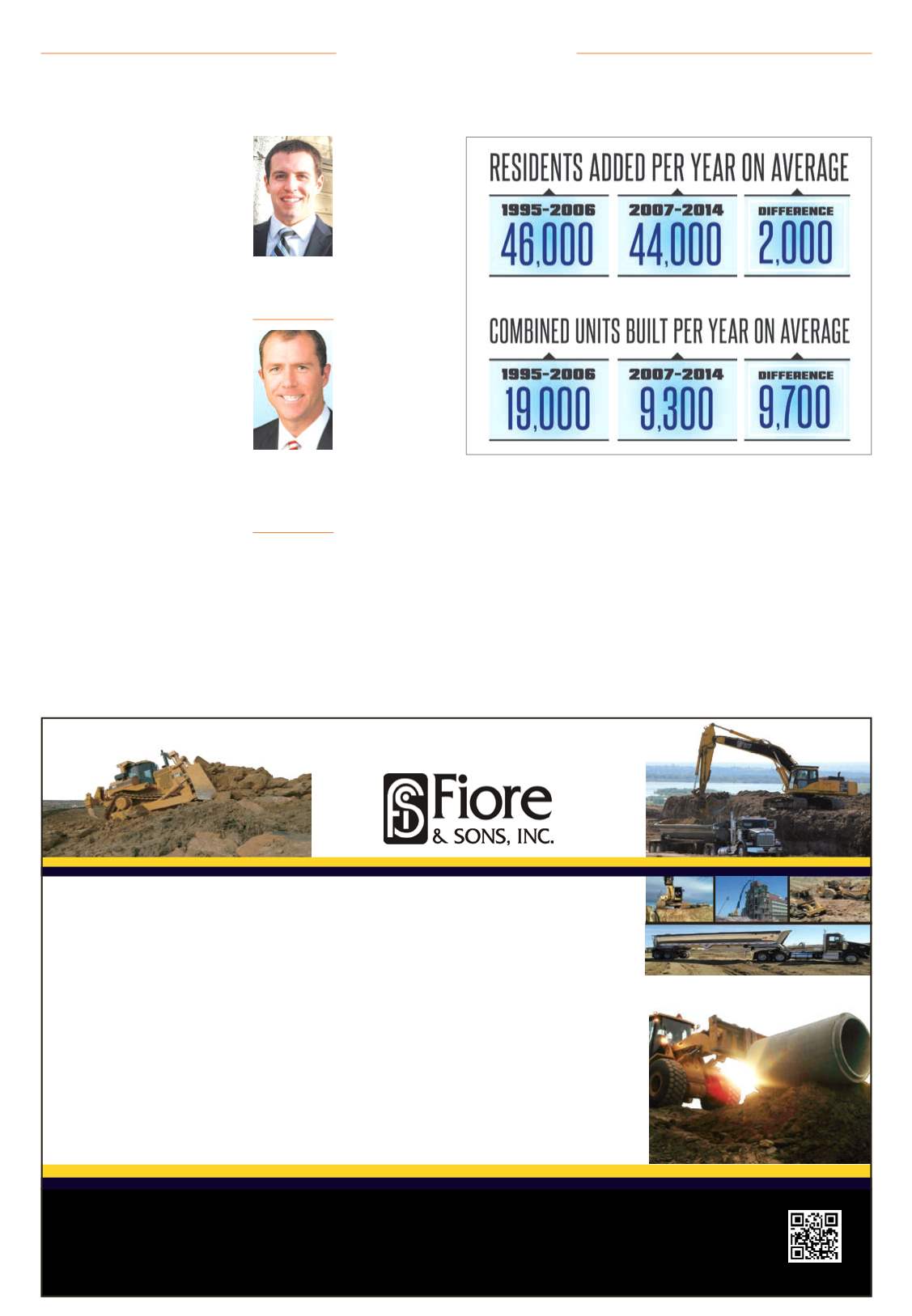

The chart provides a great visual

representation of the mysterious

“pent-up demand” we have been

hearing about over the last few years.

Focus first on the period from 1995 to

2006. During that time, the Denver

metro population grew from 2.1 mil-

lion residents to about 2.65 million

– a gain of 550,000 residents in 12

years. That equates to a population

increase of roughly 46,000 residents

per year.

During that same time period,

single-family developers and contrac-

tors delivered approximately 175,000

new homes to the market, and mul-

tifamily developers and contractors

delivered approximately 55,000 new

apartment units to the market. Total

housing deliveries combined (exclud-

ing condominium and townhome

deliveries as we were not able to

find reliable data on those markets)

equaled 230,000 units, or two-fifths

of a unit for every new person added

to the market. The

average number of

units delivered each

year during that

time period was

about 19,000.

Next, focus on the

period from 2007 to

2014. During that

time, population

grew from 2.65 mil-

lion to roughly 3

million – a gain of

350,000 residents

in eight years. That

growth breaks

down to a popula-

tion increase of

roughly 44,000 per

year – just 2,000

fewer residents per

year than Denver

had from 1995 to

2006.

Throughout that

same period, single-

family contrac-

tors only delivered

41,000 new homes

and multifamily

contractors deliv-

ered just 33,500

new apartment

units. At a total of 74,500 units (again

excluding condos and townhomes),

only one-fifth of a unit was delivered

for every new member of the popula-

tion added to our area. The average

number of units delivered each year

declined to just over 9,300 compared

to 19,000 in the previous period

reviewed.

This represents an annual shortage

of 9,700 units; multiply that out by

eight years and we could be looking

at a current shortage of 77,600 units

and growing. Add to that the fact

that the construction defect litiga-

tion environment has largely con-

strained for-sale condominium and

townhome development from 2007

to 2014, and the housing shortage

is likely much greater than demon-

strated.

When you consider that the fun-

damental driver of rental rates and

home prices is supply and demand, it

is no wonder rental rates and home

prices have reached historic highs

and are continuing to climb. As popu-

lation increases, so does demand, but

supply has failed to keep up with the

growing demand over the last eight

years. Even as construction deliver-

ies are reaching historic norms (2014

was close with over 17,000 combined

units delivered), it will take several

years above the historic norm of

19,000 units, and a significant uptick

in the condominium and townhome

construction market, to make a dent

in the current shortage of likely some

80,000 units.

So, what will stop the growth?

When do we see the downside of

this cycle? We see several factors that

could slow down the market.

Chris Geer

CEO, Haven

Property Managers

& Advisors,

Superior

Craig Stack

Vice president,

multifamily

investments,

Colliers

International,

Denver

Investment Market

Courtesy: Colliers International