by Jill Jamieson-Nichols

United Properties is

heading to the southeast

suburban submarket for

its latest big development

in the Denver area.

United Properties, in a

joint venture with Princi-

pal Real Estate Investors,

purchased 58 acres at the

southeast corner of South

Havana Street and East

Easter Avenue to develop

Dry Creek Corporate Cen-

ter, a mixed-use project

that will include approxi-

mately 650,000 square feet

of single- and multitenant

office and industrial space.

Construction will start

next spring with a 182,000-

sf multitenant office build-

ing.

Equity Office Proper-

ties Trust sold the land in

a $8.2 million deal han-

dled by Newmark Grubb

Knight Frank brokers

Jason Addlesperger and

David Lee. Mike Wafer,

also of NGKF, represented

United Properties.

“This is one of the larg-

est fully entitled parcels

of land in the heart of the

s o u t h -

east sub-

u r b a n

market,”

s a i d

K e v i n

K e l -

ley, vice

p r e s i -

dent of

U n i t e d

P r o p -

erties. “With improving

market conditions and

low supply, we’re excited

to bring this new Class A

product to market.”

The acquisition included

multifamily and hotel sites

that will be sold to outside

developers.

Dry Creek Corporate

Center is next to the Dry

Creek light-rail station,

Inverness Business Park

and Centennial Airport,

approximately 20 minutes

from downtown. With

United Properties seeking

LEED certification of all of

the buildings, the project

will include facilities for

bike commuters, including

dedicated building entries

with showers, lockers,

repair areas and bike rent-

als; a dedicated shuttle to

transport employees to

and from the light-rail sta-

tion; and pads for food

trucks, complete with cov-

ered dining areas.

“We are offering rental

rates of under $20 per

by John Rebchook

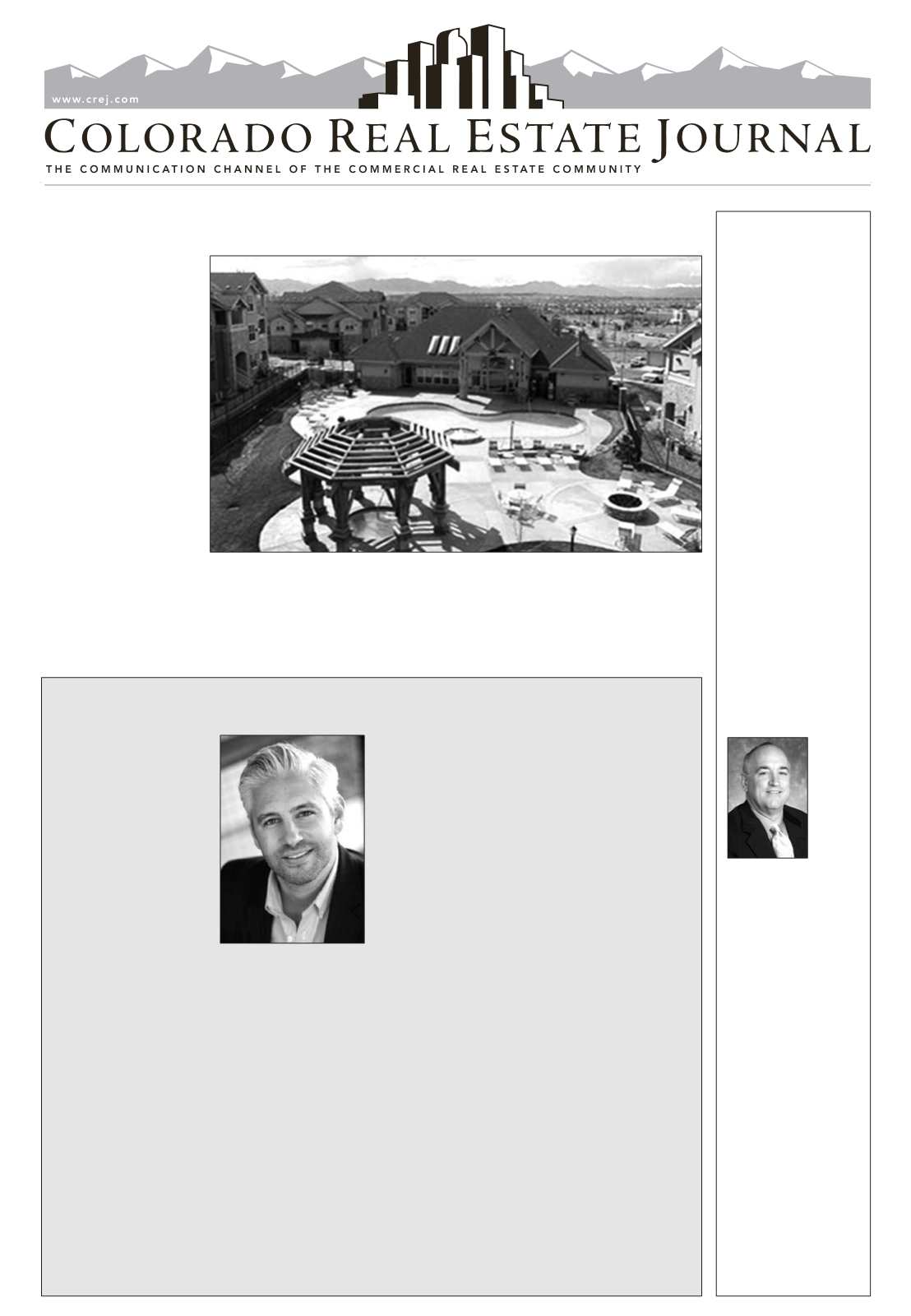

Milestone Apartments, a real

estate investment trust based

in Toronto, recently paid $40.5

million for the 221-unit Village

at Legacy Ridge in Westmin-

ster.

The community at 3850 W.

112th Ave. was sold by Den-

ver-based Corum Real Estate

Group.

The sale equates to $183,326

per unit.

Legacy Ridge was built in

2001 on a 12.3-acre site and

currently is about 97 percent

occupied.

The average monthly rent is

about $1,200 per unit.

The average rents are higher

than the average rents in the

REIT’s portfolio, according to

Milestone.

One reason the rents are

higher is because the Village

at Legacy Ridge has a higher

proportion of two- and three-

bedroom units than found in

its overall portfolio, according

to Milestone.

Milestone was drawn to the

property because of its proxim-

ity to both Boulder and down-

town Denver.

As part of the purchase,

Milestone assumed a fixed-rate

mortgage of about $23.6 mil-

lion at an interest rate of 3

percent.

The loan is fully amortized

on a 35-year schedule maturing

by John Rebchook

Matt Joblon’s company,

Cherry Creek-based BMC

Investments, is developing

the most expensive apart-

ment tower in Denver’s his-

tory.

The $108 million, 218-unit

Steele Creek apartment tower

that is under construction

at First Avenue and Steele

Street in the heart of Cherry

Creek North costs more than

$400,000 per door.

It is projected to get blend-

ed rents averaging the high-

est in Denver at about $3.50

per square foot, with pent-

house units getting far north

of that amount.

It also is the 33-year-old

Joblon’s first development.

”You really started at the

top of the ladder,” said Cary

Bruteig, owner of Apartment

Appraisers & Consultants,

when he introduced Joblon

as a development panel

member at a recent Colorado

Real Estate Journal multifam-

ily conference.

As big as it is, Steele Creek

is not the only development

on Joblon’s real estate plate.

He also has a $68 mil-

lion, 155-room hotel going

forward in Cherry Creek

North in a partnership with

Sage Hospitality and a $70

million,12-story, medical

office that will have approxi-

mately 200,000 sf planned

near the Anschutz Medical

Campus at Fitzsimons.

Steele Creek, which already

is 10 percent preleased, may

be at the top of the Denver

apartment food chain, but

Joblon has focused on the

other end of the apartment

spectrum since arriving in

the Mile High City just a few

years ago.

Since 2011, BMC (which

stands for Building Manage-

ment Co.), has purchased

3,489 apartment units for

$227.7 million in the Denver

area. Of that, $164 million

was in debt and about $64

million was in equity.

“They were all 1970s era

apartments,” Joblon said

from his office in Cherry

Creek North, where about a

dozen people work. BMC has

a total of about 70 employees,

most of them in its property

division.

Joblon, who is incredibly

analytical and risk-averse,

was bullish on the Denver

market from the get-go,

based on the same metrics

that everyone likes, such as

demand fueled by Denver’s

quality of life, job growth, its

magnetic role for millennials

and the difficulty or indiffer-

ence of young people to buy

a home, pushing them into

the rental market.

And until the latest build-

ing boom, there was a lack

of supply of apartments to

meet the growing demand,

as construction had come to

a standstill during the Great

Recession.

“But even I’ve been sur-

prised just how strong the

apartment market has been,”

he said.

It may seem like he had the

Midas touch, given that his

timing was so good.

Joblon, however, said his

path has not been without

missteps.

“I made 1,000 mistakes

along the way,” Joblon said.

However, a great market

made up for all of his mis-

takes, he said.

Even more importantly, he

learned from his errors and

engendered trust in his inves-

tors, helping him to attract

even more people willing to

write him checks with many

zeroes.

“I took full responsibility for

all my mistakes and owned up

to them,” Joblon said. “I was

ridiculously transparent.”

He didn’t have to be.

His investor pool includes

well-heeled real estate devel-

opers and investors from

New York City.

“Honestly, these guys don’t

look at the closing docu-

ments,” where they might

have discovered his momen-

tarily lapse of good judg-

ment.

One of his “doozies” was

in his first deal, an 81-unit

building purchased for $4.1

million.

He realized he only had

$600 in an account for an

operating cushion, in case

they needed more money for

any unforeseen problem.

“I sent my partners a

memo and told them it was

my mistake and I wasn’t

going to come back to them

for a capital call,” ask-

ing them to pony up more

money, he said.

Instead, he said he would

put up the money personally

at a zero percent interest rate.

Only one problem.

He didn’t have any money.

Somehow, though, he man-

aged to get a $60,000 line of

credit that he was willing to

put into the account, which

got drawn down to $200.

Cash flow after the closing

was so strong that he never

had to kick in the money.

“I tell you, I couldn’t sleep

at night,” during that period,

he said.

Matt Joblon

SECTION AA

NOVEMBER 19-DECEMBER 2, 2014

Village at Legacy Ridge recently sold.

Kevin Kelley